Global header bidding has matured into a standard monetization layer for large publishers, with adoption expanding worldwide. The ecosystem is shifting toward server-side and hybrid setups to improve performance and scale. Additionally, growing demand for SPO, transparency, and marketplace control favors flexible, white-label infrastructure solutions.

Header bidding has transformed the way digital ad inventory is bought and sold. Unlike the traditional waterfall model, it allows multiple participants to compete for an impression simultaneously, not sequentially.

Over the past several years, header bidding has evolved from a niche optimization technique into a standard monetization approach for publishers. Thus, among one million websites receiving the largest traffic, 2.2% was leveraging the header bidding technology (as of July 2025). The same applied to 7% of websites among the top 100 thousand and 10% among the top 10 thousand.

At the same time, market trends indicate that the global header bidding ecosystem is maturing, with platforms and infrastructure providers becoming a stable layer of the programmatic advertising stack.

In this guide, we will focus on how header bidding is evolving across global markets and what these changes mean for ad exchanges, SSPs (including a white-label ad exchange solution for header bidding offered by Attekmi), and the future structure of programmatic marketplaces. Read on to learn more about global header bidding market share trends.

From niche hack to global standard

The emergence of header bidding enabled publishers to bypass the limitations of the traditional waterfall model. Today, the technology has become a core component of the programmatic advertising infrastructure, allowing media owners to create more competitive auctions and giving buyers broader access to inventory.

Global adoption and market growth

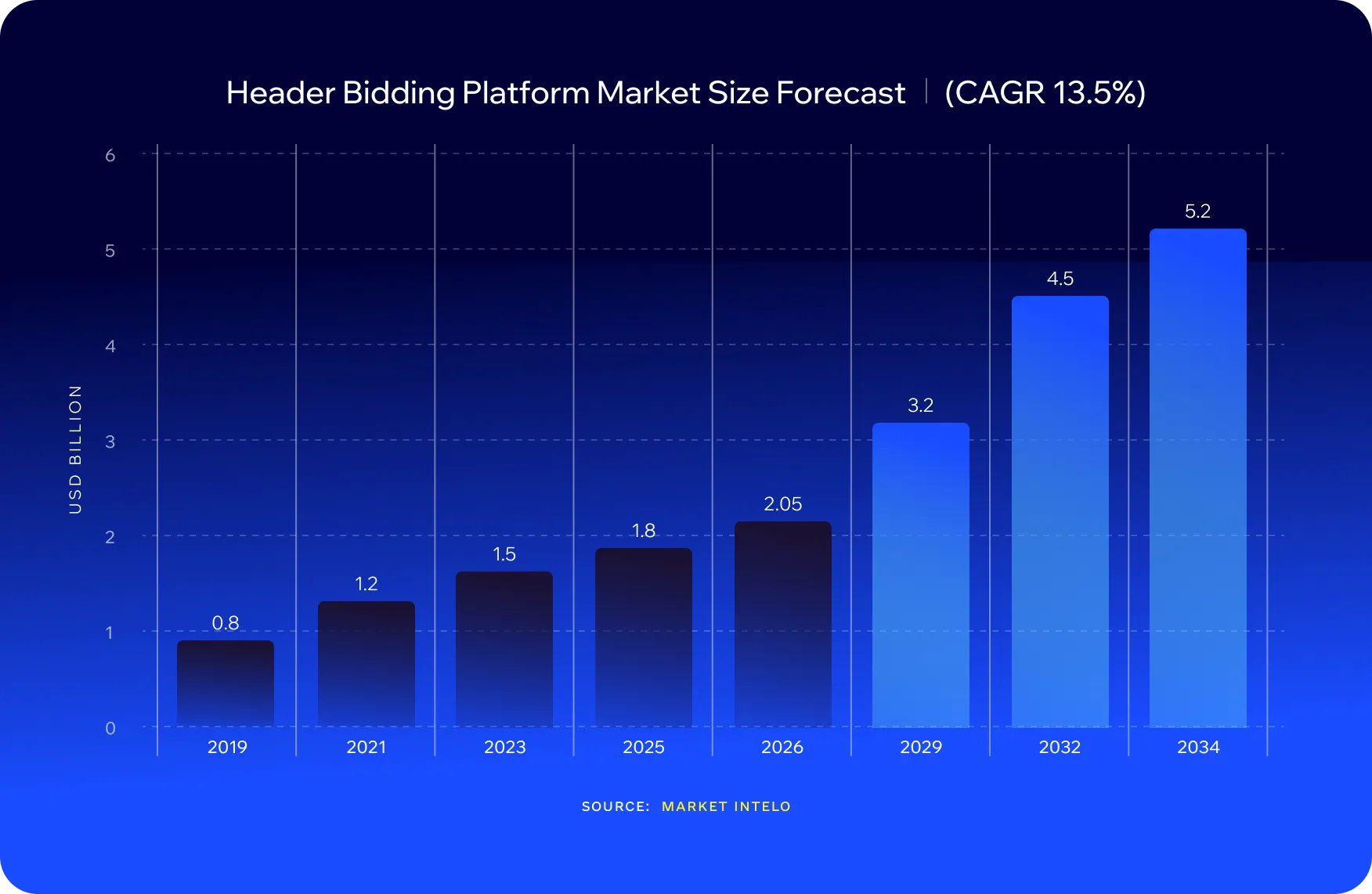

According to the research from Market Intelo, the global header bidding platform market is valued at $1.8 billion in 2025 and forecasted to surpass $5 billion by 2034:

Source: Market Intelo

This growth reflects broader adoption of programmatic infrastructure, increasing demand for transparent auctions, and publishers’ need to maximize revenue across increasingly complex digital environments.

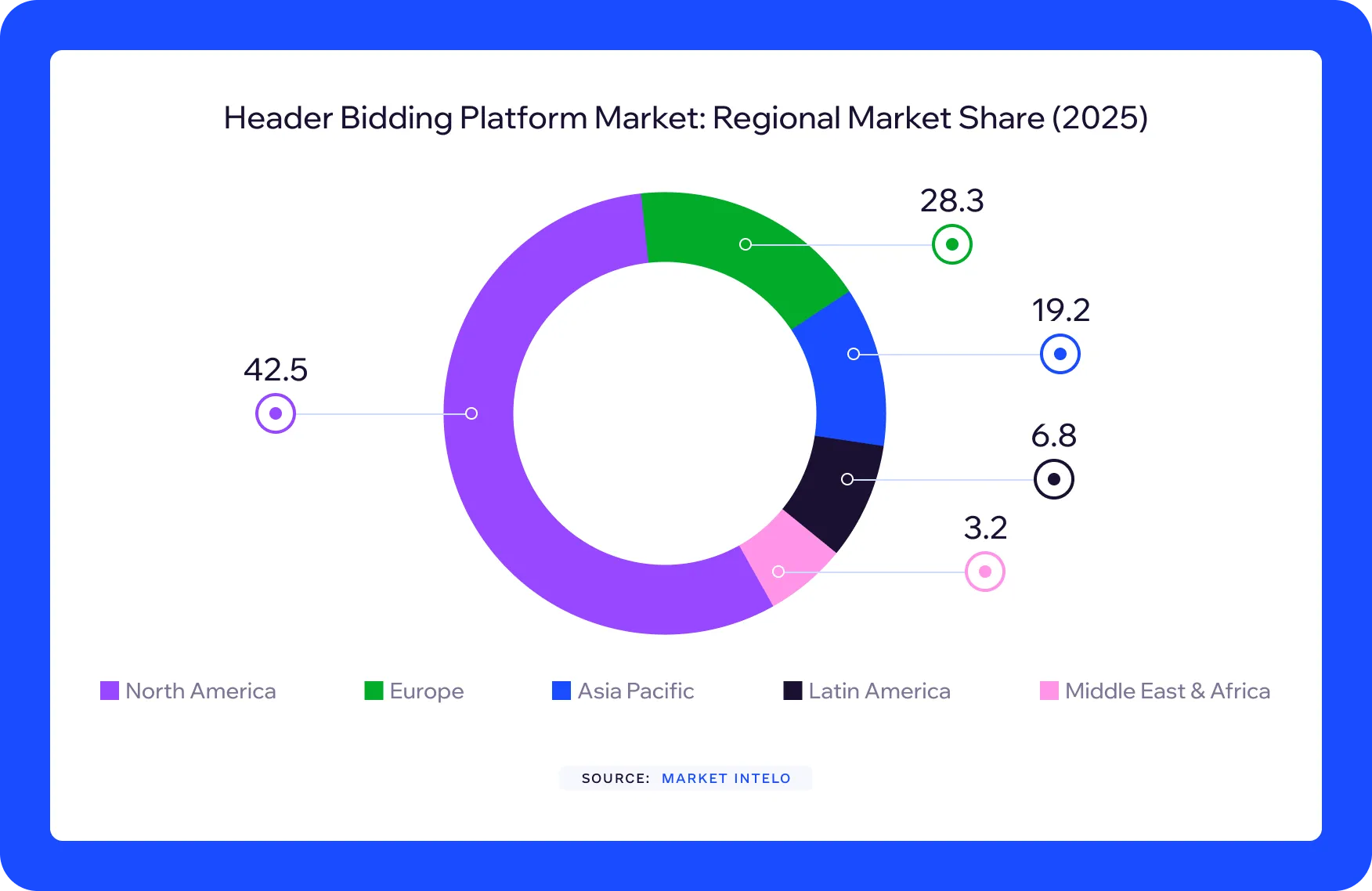

The same research indicates that North America is the leader of the header bidding platform market. However, in terms of header bidding adoption worldwide, it is not the only participant:

Source: Market Intelo

Many large publishers (and not only large) worldwide now rely on header bidding for monetization, making it a standard part of the modern ad stack rather than an optional enhancement. This is especially relevant for video and display placements.

Maturity signals: from hype to optimization

It may seem that after the initial hype, the interest in header bidding has slightly declined. However, this does not mean that publishers and advertisers do not need this technology anymore. The growing header bidding platform market proves that the trend has reached maturity. Now, the conversation has shifted from “should we implement header bidding?” to “how do we optimize partners, timeouts, and server‑side setups?”

As for ad exchanges, they must now compete by providing stronger marketplace capabilities, better bid performance, actionable data, and infrastructure that helps publishers achieve better outcomes. Offering classic waterfall bidding is no longer enough. In a robust header bidding ecosystem, success heavily depends on the ability to deliver measurable value within every auction.

Architecture trends: client-side, server-side, and hybrid

Obviously, client-side vs server-side header bidding trends are also worth mentioning, as well as hybrid header bidding growth. Let’s take a closer look at the details.

Client-side remains the transparency benchmark

Client-side header bidding remains an important part of the programmatic ecosystem because it provides publishers with greater visibility into the auction process. With solutions such as Prebid.js running directly in the browser, media owners can see individual bidder responses, control auction parameters, and maintain relationships with demand partners.

For many web publishers, this approach offers benefits like transparency and identity matching. The auction happening in the user’s browser enables better access to available user signals and cookie-based targeting capabilities. This can contribute to stronger bid values in certain environments.

However, the industry is becoming more selective about client-side implementations. Instead of adding as many bidders as possible, publishers are increasingly focusing on smaller groups of consistently high-performing partners. This reflects a broader shift toward auction efficiency: reducing unnecessary latency, improving page experience, and prioritizing demand quality over quantity.

Server-side growth for performance and scale

Server-side header bidding addresses some of the limitations of browser-based auctions by moving the bidding process away from the user’s device. Instead of each demand partner receiving a separate browser request, the publisher sends a single request to a server-side platform. Then, the request is distributed further to multiple demand sources.

This architecture plays an especially critical role for high-traffic publishers, mobile environments, and organizations managing large numbers of global demand relationships. By reducing the number of browser calls, server-side setups can improve page speed, support larger auctions, and simplify technical processes.

The adoption of server-side header bidding continues to grow as publishers look for ways to balance monetization performance with user experience. The trend is especially visible in areas such as video, CTV, and mobile app inventory, where latency limitations and technical complexity make browser-based auctions more challenging.

Hybrid configurations becoming the norm

Rather than choosing between client-side and server-side approaches, many publishers are adopting hybrid architectures. These setups typically keep a limited number of premium bidders in the client-side auction, while moving additional demand partners to server-side infrastructure.

This model allows media owners to benefit from both approaches at once. High-value partners can compete directly with maximum visibility, while the broader demand ecosystem can participate without creating excessive browser load or affecting user experience.

Hybrid configurations reflect the growing maturity of header bidding. Publishers are no longer searching for a single universal setup but are building customized auction environments based on inventory type, audience, geography, and monetization goals.

For exchanges, this means that they must perform effectively across multiple integration models. A competitive exchange should be capable of operating as a client-side bidder while also supporting server-side connections and scalable auction infrastructure. This creates a strategic opportunity for white-label exchanges and marketplace platforms, which can serve as centralized server-side auction layers connecting multiple publishers with diverse demand sources.

Global header bidding market share and regional nuances

As header bidding has become a core component of programmatic infrastructure, competition within the ecosystem has evolved. Now, the question is not about whether exchanges can participate in publisher auctions. It is about how effectively they can compete for impressions.

Concentration and competition among exchanges

Major exchanges and SSPs often account for a substantial portion of publisher monetization, particularly in high-volume environments like web and CTV (only in the USA, CTV ad spend is expected to surpass $52 billion by 2029).

However, the market is not limited to a few big players. A long tail of specialized exchanges remains valuable by providing access to unique audiences, regional demand, specific content categories, and emerging inventory formats. Many publishers use a combination of large-scale platforms that provide reach alongside smaller solutions that deliver additional demand and competition.

This approach has become a common pattern in header bidding setups. Media owners typically maintain a group of trusted partners while adding specialized sources where they can improve auction performance. This is especially relevant in areas like mobile and CTV, where inventory characteristics, audience behavior, and buyer demand can vary significantly across markets.

Regional differences in adoption and partner mix

Although header bidding adoption is expanding globally, implementation patterns differ between regions. Local advertising ecosystems, regulatory requirements, and advertiser demand influence how media owners build their auction strategies and select technology partners.

In more mature programmatic markets like North America and Europe, header bidding penetration is high. Many premium publishers there rely on advanced hybrid setups that combine client-side and server-side approaches. These markets usually feature a mix of global platforms and regional specialists that provide additional competition, local market knowledge, and access to specific advertiser segments.

In developing markets such as APAC and LATAM, adoption is growing rapidly as publishers and advertisers increase their use of automated buying. For instance, the Latin America programmatic advertising market is forecasted to exceed $236 billion by 2030. However, the preferred partner mix can differ significantly from one region to another. Local demand relationships, infrastructure availability, privacy regulations, and differences in advertiser behavior shape which exchanges become valuable auction participants.

These regional differences explain why global header bidding strategies cannot rely on a universal approach. Ad exchanges and white-label marketplace providers need to consider local requirements when expanding into new markets, including infrastructure placement, latency optimization, compliance capabilities, and relationships with regional publishers and buyers.

How global header bidding trends are reshaping ad exchanges

As for the header bidding impact on ad exchanges, there are three main trends to consider. Here they are.

Exchanges moving from “endpoint” to “marketplace layer”

In the early stages of header bidding adoption, exchanges mainly acted as individual endpoints within a publisher’s auction. A wrapper would send bid requests to multiple partners, and each exchange would compete independently for impressions. While this model increased competition compared with the traditional waterfall, the role of each exchange was relatively limited.

As server-side and hybrid architectures become more common, the role of exchanges is expanding. Instead of simply responding to bid requests, exchanges increasingly function as centralized marketplaces that manage auctions, connect multiple demand sources, and provide publishers with additional control over monetization workflows.

This shift is also enabling more organizations to operate their own marketplace infrastructure through white-label exchange solutions. Publishers can create customized auction environments while still connecting to external demand sources.

The competitive advantage now belongs to platforms that offer comprehensive marketplace capabilities rather than basic bidding functionality. Features such as deal management, supply path controls, analytics, and customizable auction logic help exchanges become strategic partners in the monetization process.

SPO, transparency, and log‑level analytics pressure

Header bidding growth is closely connected with the industry movement toward supply path optimization and greater marketplace transparency. Buyers and sellers look for shorter and cleaner supply paths. They strive for visibility into how impressions move through the ecosystem and which partners provide real value.

This creates new expectations for exchanges. Detailed reporting, log-level analytics, transparent fee structures, and flexible routing options are becoming important requirements.

Header bidding increases this pressure because it gives publishers more flexibility to test, compare, and replace partners. When demand sources can be added or removed more easily, exchanges need clear performance advantages.

For white-label exchange providers like Attekmi, this creates an opportunity to position their platforms as SPO-friendly infrastructure. By giving publishers more control over auction paths, partner relationships, and data visibility, these solutions can help reduce unnecessary complexity while maintaining access to competitive demand.

CTV and app header bidding accelerating server-side innovation

The growth of CTV and in-app advertising (in-app display formats account for more than 70% of mobile programmatic impressions) is the driving force behind the innovation of server-side auction technologies. Unlike web environments, these channels often have device limitations, stricter performance requirements, and workflows that make browser-based header bidding simply impractical.

In CTV and in-app environments, server-side bidding and mediation approaches provide the scalability needed to connect multiple demand sources without adding excessive technical complexity. This has made strong server-side infrastructure a key competitive factor for exchanges planning to expand into these rapidly growing segments.

Note that as adoption increases, the definition of header bidding is becoming broader. The ecosystem now includes not only traditional web auctions but also CTV header bidding, in-app bidding, and other server-driven marketplace models. For exchanges, the opportunity is significant. Platforms that can support multiple environments, formats, and auction models have much higher chances of becoming long-term infrastructure partners.

What global header bidding trends mean for publishers and networks

As header bidding becomes a mature part of programmatic infrastructure, publishers need to rethink how they approach monetization optimization. Here are a few recommendations for you.

It is time to think in architectures, not just partners

In the early days of header bidding, optimization often focused on adding more demand partners to increase competition. However, nowadays, effective revenue improvements come from architectural decisions.

Factors such as the balance between client-side and server-side bidding, partner prioritization, timeout settings, auction logic, and inventory routing can have a significant impact on monetization efficiency. A smaller, well-optimized setup can often outperform a larger but inefficient one.

Note that exchanges are becoming an important part of this architecture. Their value depends not only on the demand they provide but also on how effectively they integrate into your monetization strategy.

Testing and measurement become continuous

Keeping an eye on the global header bidding market share trends is helpful, but each of your decisions should still be data-driven. Approaches such as A/B testing and multi-armed bandit testing allow you to evaluate changes based on actual performance data. This requires exchange platforms to provide strong reporting capabilities, transparent performance metrics, and integrations with existing analytics systems.

White-label exchanges can simplify the process by providing a centralized control layer for testing and standardizing header bidding setups across multiple websites, applications, and regions. Instead of managing separate configurations, you can use one platform to optimize auction strategies at scale.

Owning more of the exchange layer is now a real option

The evolution of header bidding has created new opportunities for publishers. Businesses that previously relied on third-party marketplaces can now consider operating their own branded exchange or SSP environment through white-label infrastructure.

In this model, a company’s marketplace can participate in header bidding auctions like any other participant. However, behind that integration is a customized exchange layer that the organization controls. This enables greater flexibility over auction rules, data access, monetization strategies, and partner management.

For publishers with significant inventory volumes or specific audiences, owning more of the exchange layer can provide strategic advantages. It allows for reducing dependency on external platforms while creating a more tailored marketplace environment.

Attekmi’s white-label solution supports a range of ad formats and environments, offers advanced targeting, filtering, and analytics capabilities, and is fully customizable. Using it, you can gain greater control over your header bidding monetization processes and join the evolving programmatic ecosystem in a streamlined manner.

Conclusion

Global header bidding market share trends show how far the technology has evolved. What started as an experiment turned into a globally adopted component of programmatic infrastructure.

Client-side header bidding continues to play an important role where transparency, control, and identity signals are priorities. At the same time, server-side and hybrid configurations are expanding as publishers look for greater scalability, lower latency, and support for complex environments.

The exchange landscape is also becoming more competitive. While market share is consolidating around a mix of global and regional exchanges, differentiation increasingly comes from supply path transparency, data accessibility, auction efficiency, and the ability to deliver real value.

Additionally, the growth of CTV and app header bidding will further accelerate innovation on the server-side and marketplace layers. Exchanges that can support flexible architectures, transparent workflows, and scalable auction management will have the highest chances to succeed in the next stage of programmatic evolution.

Ready to launch your own monetization platform? Just contact the Attekmi team.

FAQ

Header bidding has moved from experimentation to a robust infrastructure layer. While growth rates have stabilized in mature markets, adoption continues expanding globally (especially across emerging regions, CTV, mobile, and server-side environments). The focus is shifting from implementation to optimization and efficiency.

Client-side header bidding remains important for transparency, control, and identity-based targeting. However, server-side and hybrid setups are growing as publishers prioritize performance, scalability, and reduced latency. Many advanced publishers now combine both approaches, keeping premium bidders client-side while moving additional demand server-side.

Ad exchanges are evolving from simple bidding endpoints into marketplace infrastructure providers. They must offer strong auction performance, transparency, analytics, supply path controls, and flexible integrations. Success increasingly depends on the value an exchange adds within the publisher’s architecture, not just access to demand.

CTV and in-app environments accelerate the need for server-side capabilities because browser-based auctions are often impractical. Exchanges need scalable infrastructure, support for multiple formats, efficient auction processing, and strong integrations with mediation and server-side workflows to compete in these growing segments.

A publisher or network should consider a white-label exchange when it has significant inventory volume, complex partner relationships, or a need for greater control over monetization. It can help standardize auctions, improve transparency, manage demand relationships, and create a customized marketplace without building infrastructure from scratch.